What is Duty Drawback

Duty drawback can put money back in your pocket when you have goods that have been previously imported to the U.S. and then exported. This process can be complicated to navigate so talking with a Licensed Broker that is a Duty Drawback Specialist about this program can lead to greater success and give you the largest duty return possible.

What is Duty Drawback?

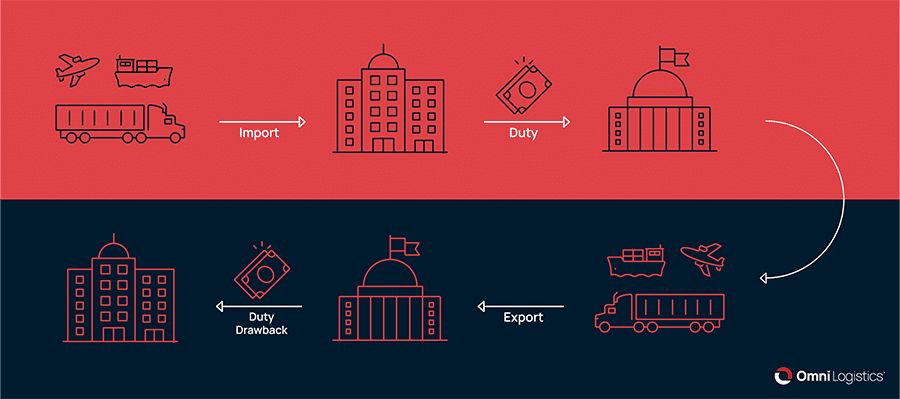

A drawback is a refund of customs duties and taxes paid on imported merchandise that is later exported or used in the manufacture of exports.

In the world of U.S. Customs, duty drawback is recognized as a lawful way to allow importers the ability to reduce the impact of tariff duties on imported items that will then be exported. U.S. Customs and Border Protection (CBP) defines duty drawback as “…the refund, reduction or waiver in whole or in part of customs duties assessed or collected upon importation of an article or materials which are subsequently exported.”

What are the benefits of duty drawback?

Duty drawback refunds 99% of duties (including 301 duty), taxes, and fees paid on imported products, if those products, comparable products, or products produced from the imported product are exported within five years. Thanks to TFTEA, for substitution, the imported and exported products do not have to be the exact same products if they are the same 8-digit USHTS.

Today, duty drawback provides extensive refund opportunities for any business that imports and exports in the U.S. This means more cash flow to put back into your business.

What are the types of Duty Drawback?

- Manufacturing Direct Identification Drawback

When duty-paid imported material is used to manufacture a product, which is later exported from the United States, U.S. import duty may be recovered. It is, however, necessary to trace the duty-paid imported material through manufacture and export.

- Manufacturing Substitution Drawback

When imported duty-paid, duty-free or domestic material of the same kind and quality as the imported duty-paid designated material is used to produce the exported product, U.S. import duty may be recovered. This is true even when none of the designated merchandise may have been used to produce the exported articles.

- Unused Merchandise Direct Identification Drawback

When material is imported duty-paid and later exported unused, U.S. import duty may be recovered. It is, however, necessary to trace the duty-paid imported material through to export.

- Unused Merchandise Substitution Drawback

When unused material, which is commercially interchangeable with the imported duty-paid material, is exported, U.S. import duty may be recovered. It is important to note that, under the provision, the imported duty paid material does not have to be exported if the substituted merchandise is.

- Rejected Merchandise Drawback

Your business may file a claim for drawback on imported material that is later exported, and which does not conform to sample or specifications, has been shipped without the consent of the consignee, or has been determined to be defective as of the time of importation.

Claimants under manufacturing or unused merchandise drawback may, if approved, file retroactively, provided that the drawback claims are filed within three years of the date of export. For many companies, this first recovery of duty can be quite large.

Guidelines

Duty drawback creates a tremendous opportunity for importers and exporters to recover duties and taxes previously paid on imported merchandise that will be exported or destroyed. The process can be complicated with a few guidelines to keep to in mind.

- As of Feb. 24, 2019, duty drawback claims must be filed in the Automated Commercial Environment (ACE) according to the requirements of the 2015 Trade Facilitation and Trade Enforcement Act (TFTEA).

- 8-digit HTS substitution will be used to match claims opposed to commercial interchangeability; if the 8-digit classification starts with “other”, then the matching will be based on 10-digit HTS classification

- Drawback time frames will be 5 years (previously three years) from import to filing a claim

- Drawback record keeping will be 3 years from liquidation of the claim

- Claims on Merchandise Processing Fee and Harbor Maintenance Fee will be available for manufacturing drawback in addition to unused drawback

- Business records will be used to track transfers rather than the Certificates of Delivery

- The duty claimed for manufacturing substitution will be based on the lesser of: (1) the duties paid on the imported merchandise and (2) the duties paid on the substituted merchandise if it were imported

- The duty claimed for unused substitution will be based on the lesser of: (1) the duties paid on the imported merchandise and (2) the duties paid on the exported article if it were imported

How can I reduce duties and taxes on imports?

A U.S. Licensed Customs Broker with comprehensive knowledge and experience can help you with the following services, as it relates to your duty drawback:

- Preparation and Submission of Manufacturer’s Drawback Ruling

- Preparation and Submission of all requests for Special Privileges (Accelerated Payment, Waiver of Prior Notice, One-Time Waiver of Prior Notice)

- Preparation and Filing of all Duty Drawback Claims

- On-Site follow-up with U.S. Customs and Border Protection to ensure prompt payment of Duty Drawback Claims

- Duty Drawback Audit Services

- Record Retention Management

- Complete Management of the business’ Duty Drawback account